Secured credit cards without hard inquiry are becoming an increasingly popular option in 2026 — especially for seniors and credit rebuilders who want to protect their credit score from additional damage.

For seniors concerned about protecting their score, secured credit cards without hard inquiry can offer a more controlled entry point.

Another application means another inquiry. Another inquiry could mean another drop in your score. For many seniors and credit rebuilders in 2026, the fear isn’t just rejection — it’s making things worse.

That’s where secured credit cards that don’t require a hard credit check enter the conversation.

But here’s the important clarification: “no credit check” is often misunderstood. Some cards avoid a hard inquiry, but still perform identity and banking verification. Others use soft prequalification models before approval.

In this guide, we’ll clarify what “no hard inquiry” really means, who should consider these cards, what approval odds actually look like, and how to use them strategically to graduate to unsecured credit.

No hype. No shortcuts. Just clarity.

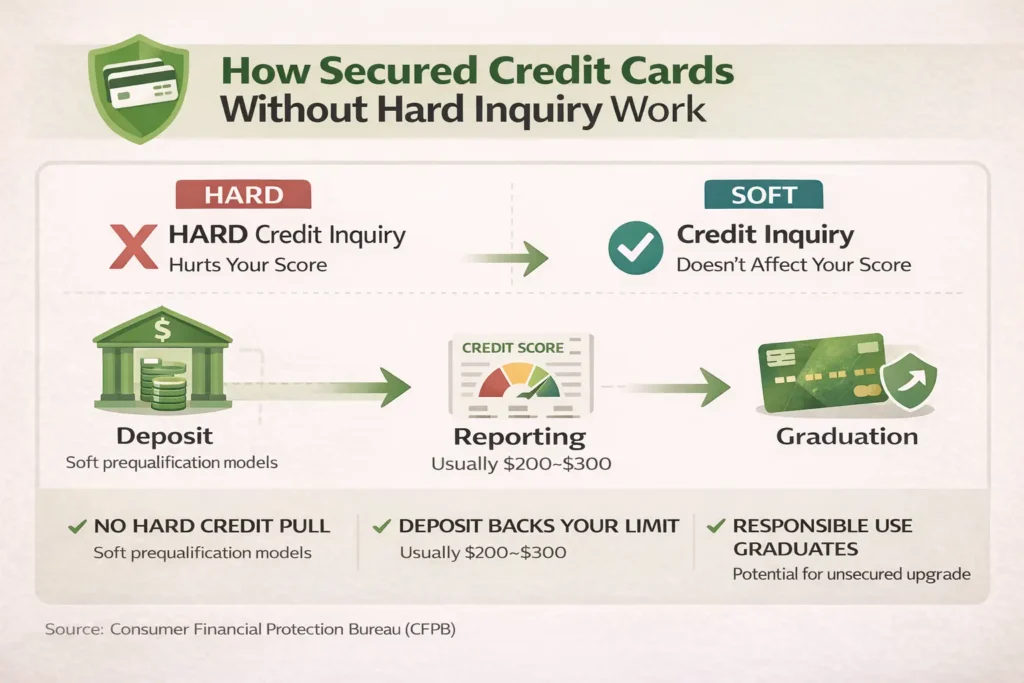

What Does “No Credit Check” Really Mean?

Before choosing any secured card, it’s essential to understand the mechanics behind credit inquiries.

Hard Inquiry

A hard inquiry occurs when a lender formally pulls your credit report during an application.

- It can lower your score by a few points

- It remains visible for up to two years

- Multiple hard inquiries signal risk

Hard inquiries matter most when your score is already below 600.

The Consumer Financial Protection Bureau provides additional guidance on how credit card inquiries and reporting work in practice.

Soft Inquiry

A soft inquiry does not impact your credit score.

Soft pulls are used for:

- Prequalification checks

- Promotional offers

- Background identity verification

You may not even see them immediately on your credit monitoring tools.

Prequalification Models

Some secured card issuers allow you to check eligibility using a soft pull before you formally apply.

This reduces risk. You can see potential approval odds without harming your score.

However, if you proceed with the full application, a hard inquiry may still occur — unless the issuer explicitly states otherwise.

Risk Models in 2026

In 2026, many secured card issuers rely less on traditional FICO thresholds and more on:

- Income stability

- Identity verification

- Banking history

- Fraud screening

Because secured cards require deposits, the risk model shifts away from pure credit scoring.

Understanding these distinctions increases your approval strategy precision — and strengthens your financial control.

Who Should Consider a Secured Credit Cards Without a Hard Inquiry?

Not everyone needs to avoid a hard inquiry.

But certain situations make it wise.

1️⃣ Recent Denial

If you were recently denied for unsecured credit, applying again immediately may trigger another inquiry without improving odds.

Soft-check secured options reduce that risk.

2️⃣ Score Under 600

When scores fall below 600, every inquiry matters more.

Minimizing additional hard pulls protects stability.

3️⃣ Thin Credit File

If you have limited credit history — perhaps after retirement or years of debt-free living — secured cards can help establish activity without aggressive underwriting.

4️⃣ Banking History Issues

Some applicants struggle more with ChexSystems (banking reports) than credit scores.

Certain secured cards rely less on traditional bureau pulls and more on identity and deposit verification.

If you’re unsure where you stand, reviewing our Secured Credit Cards for Seniors (2026 Complete Guide) can provide additional context before applying.

The 3 Best Secured Credit Card Categories in 2026

Rather than naming specific issuers, we’ll focus on categories that consistently offer low-risk entry points.

1️⃣ Low-Deposit Secured Cards ($200–$300)

These are the most common entry-level secured cards.

Features typically include:

- Minimum deposit between $200–$300

- Reporting to major credit bureaus

- Moderate annual fees (or none)

Some issuers within this category avoid hard inquiries entirely, relying instead on deposit-based underwriting.

This is often the safest first step.

For more detail, see our breakdown of $200 secured cards for seniors.

2️⃣ Secured Cards with Soft Prequalification

These cards allow applicants to check eligibility through a soft pull before submitting a formal application.

Benefits include:

- Reduced application anxiety

- Greater transparency

- No immediate score impact

If prequalified, the final approval process may or may not require a hard inquiry — always verify terms.

This category works well for cautious rebuilders.

3️⃣ Secured Cards That Don’t Pull from All Three Bureaus

Some issuers pull from only one credit bureau rather than all three.

This reduces visibility across your entire credit file.

However, reporting should still go to all three bureaus for rebuilding effectiveness.

This subtle difference matters when protecting your profile from widespread inquiry impact.

How to Compare Secured Credit Cards Without Hard Inquiry

Not all secured credit cards without hard inquiry are structured the same way.

Before choosing, compare these factors carefully:

Deposit Flexibility

Some issuers allow deposits above the minimum to increase your credit limit. Others fix the limit strictly at $200 or $300.

Reporting Frequency

To build credit effectively, the card must report to all three major credit bureaus monthly.

Graduation Policy

The best secured cards without hard inquiry include automatic review after 6–12 months for potential upgrade to unsecured status.

Fee Transparency

Look for clear terms. Avoid cards with excessive processing or hidden maintenance fees.

Comparison reduces regret.

And regret often damages rebuilding momentum.

What Approval Odds Really Look Like

Let’s be realistic.

Secured cards have higher approval rates than unsecured cards — often significantly higher.

But they are not automatic.

Approval depends on:

- Verified identity

- Valid Social Security number

- Deposit funding

- No active fraud alerts

- No unresolved legal restrictions

If you can provide the deposit and pass identity verification, approval odds are generally strong — even with scores under 580.

That said, no issuer guarantees approval.

Strategic patience beats rushed applications.

When Avoiding a Hard Inquiry Actually Makes Sense

Not every applicant needs to avoid a hard pull. In many cases, a single inquiry only reduces a score by a few points.

However, secured credit cards without hard inquiry make the most sense when:

• You’ve had two or more recent hard pulls in the last 90 days

• Your score is below 580

• You’re preparing for a major loan application

• You’re rebuilding after a recent delinquency

In these situations, preserving score stability matters more than marginal reward differences.

A no hard inquiry secured card reduces volatility during a fragile rebuilding phase.

That stability is often more valuable than chasing faster approvals.

Risks and Hidden Fees to Watch For

Authority requires acknowledging risk.

Here are red flags:

High Processing Fees

A $200 deposit should not come with $100 in non-refundable fees.

Monthly Maintenance Charges

Recurring monthly charges erode your rebuilding progress.

Excessive APR

While you should always pay in full, extreme APR structures signal poor long-term design.

No Graduation Path

Some secured cards never transition to unsecured status.

Graduation flexibility increases long-term value.

Understanding these elements prevents “bad credit traps.”

How to Use a Secured Card to Graduate to Unsecured

A secured card is not the final destination.

It’s a bridge.

0–3 Months

- Keep utilization under 30%

- Pay in full

- Establish autopay

3–6 Months

- Maintain perfect payment history

- Avoid new applications

- Monitor score movement

6–12 Months

- Look for automatic graduation reviews

- Consider applying for low-fee unsecured card

- Do not close secured card prematurely

Account age contributes to credit strength.

Structure — not speed — determines success.

Frequently Asked Questions

Do secured cards without hard inquiries build credit?

Yes — if they report to major credit bureaus.

Will avoiding a hard inquiry protect my score significantly?

It protects it marginally. Hard inquiries typically reduce scores by a few points, but multiple inquiries compound risk.

Can you get approved with only Social Security income?

Yes. Stable retirement income qualifies for most secured applications.

How long should you keep a secured card?

At least 6–12 months, often longer to preserve account age.

Are “no credit check” cards safe?

Some are legitimate. Others rely on heavy fees. Always read terms carefully.

Realistic Credit Score Improvement Timeline

Using secured credit cards without hard inquiry does not create overnight transformation.

Here’s what realistic progress looks like:

Month 1–3

On-time payments begin strengthening payment history — the largest scoring factor.

Month 3–6

Utilization improvements begin reflecting in measurable score changes.

Month 6–12

Many rebuilders see increases between 20–60 points depending on starting profile.

Consistency matters more than speed.

Secured cards work best when treated as structured financial tools — not emergency credit lines.

How Secured Credit Cards Without Hard Inquiry Fit Into a Long-Term Plan

Secured credit cards without hard inquiry should not be viewed as shortcuts.

They are phase-one tools in a broader credit strategy.

Phase 1 – Stabilize

Open one secured card. Keep utilization below 30%. Pay in full monthly.

Phase 2 – Strengthen

After 6 months, monitor score changes and request a credit limit increase if available.

Phase 3 – Transition

Once your score reaches the mid-600s, consider applying for a no-annual-fee unsecured card while keeping your secured account open.

Used properly, secured credit cards without hard inquiry create a stable foundation for long-term credit growth — especially for seniors managing fixed retirement income.

Strategic Perspective

A no-hard-inquiry secured card is not a loophole.

It’s a structured risk-management tool.

For seniors and rebuilders in 2026, the objective is simple:

Protect your score.

Build history consistently.

Graduate responsibly.

Credit rebuilding is not about urgency.

It’s about controlled momentum.

And controlled momentum builds lasting financial stability.