No-annual-fee credit cards for bad credit can be one of the safest ways to rebuild your credit score in 2026. A low credit score can feel like a financial lock on your life.

It affects everything—from renting an apartment to qualifying for affordable insurance or loans.

In 2026, rebuilding credit is still very possible, but only if you choose the right tools.

The wrong card can slow you down or cost you money you don’t have.

This guide focuses on no-annual-fee credit cards that are designed to help you rebuild your credit safely and efficiently.

Why Rebuilding Credit Is Harder in 2026

Lenders have become more cautious in recent years.

Missed payments, medical debt, or high balances can impact your score for longer than many people expect.

At the same time, many “credit repair” offers promise fast results but deliver little value.

That’s why using a legitimate credit card—responsibly—is still one of the most reliable ways to rebuild your score.

Why Credit Rebuilding After 55 Requires a Different Strategy

Rebuilding credit later in life is different from rebuilding at 25.

Many seniors are not trying to qualify for luxury cards or travel rewards.

The focus is stability:

- Lower insurance premiums

- Easier apartment approvals

- Better loan terms

- Financial flexibility in retirement

For retirees living on Social Security or fixed income, predictability matters more than rewards.

That’s why no-annual-fee structures are often the safest entry point.

If your score is below 620, you may also want to compare secured options in our guide:

Best Secured Credit Cards for Seniors with a $200 Deposit (2026 Guide)

Why No-Annual-Fee Cards Matter More for Seniors

For retirees, every recurring expense matters.

An annual fee may seem small—$39 or even $59—but over several years, it reduces the financial benefit of rebuilding credit.

No-annual-fee cards remove that pressure. They allow seniors to:

- Keep accounts open long-term

- Build account age without ongoing cost

- Focus on utilization and payment consistency

When rebuilding credit after retirement, minimizing fixed costs is just as important as improving your score.

If you’re unsure whether a secured or unsecured option is better for your situation, review our guide on Best Credit Cards for Seniors with Bad Credit (2026).

What Makes a Credit Card Good for Credit Rebuilding?

Before jumping into specific cards, it helps to know what actually improves your credit score.

A good rebuilding card should:

- Report activity to all three credit bureaus

- Have no annual fee

- Offer a reasonable path to credit limit increases

Most importantly, it should encourage responsible use, not long-term debt.

Understanding the Difference Between Secured and Unsecured Rebuilding Cards

Before choosing a no-annual-fee card, it’s important to understand the structure behind it.

Secured cards require a refundable deposit and are usually easier to qualify for.

Unsecured rebuilding cards do not require a deposit but may have stricter approval standards.

If your score is below 600, a secured structure may offer more predictable approval.

If your score is above 620, unsecured no-annual-fee options become more realistic.

For a full breakdown of secured options, see:

Secured Credit Cards for Seniors (2026 Complete Guide)

Best No-Annual-Fee Credit Cards for Bad Credit in 2026

1. Capital One Platinum Credit Card

Best for: Fair credit or limited credit history

This card is a popular starting point for rebuilding credit.

There’s no annual fee, and Capital One is known for consistent credit bureau reporting.

You won’t earn rewards, but that’s not the goal here.

The focus is rebuilding trust with lenders.

2. Discover it Secured Credit Card

Best for: Strong credit-building structure

This secured card requires a refundable deposit, but it offers real advantages.

Discover reviews accounts regularly and may transition you to an unsecured card.

It also earns cash back, which is rare for secured cards.

3. OpenSky Secured Visa

Best for: No credit check approval

This card does not require a credit check at all.

Approval is based solely on your security deposit.

It’s especially useful for people recovering from serious credit setbacks.

4. Petal 1 Visa Credit Card

Best for: Thin credit files or young rebuilders

Petal looks beyond traditional credit scores.

It considers income and cash flow, making it more accessible for some applicants.

There’s no annual fee, and responsible use can lead to higher limits.

5. Chime Credit Builder Card

Best for: Credit beginners who want simplicity

This card works differently than traditional credit cards.

You spend money you’ve already deposited, which reduces the risk of overspending.

Payments are reported to credit bureaus, helping build a positive history.

Quick Comparison Table

| Card | Best For | Key Benefit | Ease of Access |

|---|---|---|---|

| Capital One Platinum | Fair credit | No annual fee, trusted issuer | Moderate |

| Discover it Secured | Structured rebuilding | Cash back + upgrade path | Moderate |

| OpenSky Secured Visa | Bad credit | No credit check | High |

| Petal 1 Visa | Thin credit | Alternative approval model | Moderate |

| Chime Credit Builder | Beginners | No debt risk | High |

Which Card Type Is Right for Your Current Credit Score?

Choosing the wrong type of card can slow your progress.

Use this quick reference:

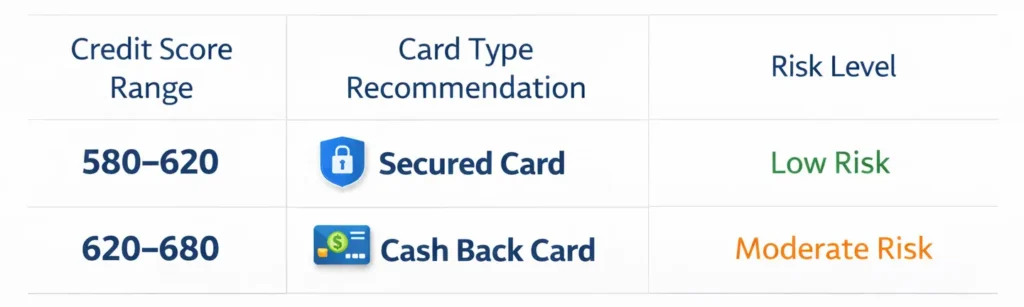

Score Below 580

→ Secured card with refundable deposit

Score 580–620

→ Secured or alternative approval unsecured card

Score 620–680

→ No-annual-fee unsecured rebuilding card

Score Above 680

→ Consider moving toward low-interest or rewards structures

Matching the card to your score prevents unnecessary denials and extra hard inquiries.

Choosing the right no-annual-fee credit cards for bad credit depends on your current score range and approval odds.

Who Should Consider No-Annual-Fee Cards?

How These Cards Actually Improve Your Score

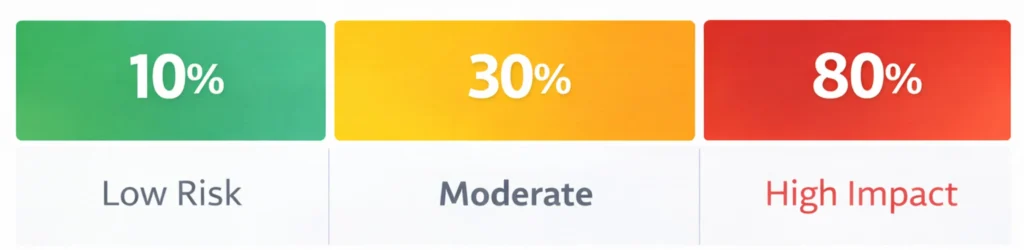

A credit card improves your score through behavior, not approval.

Three key scoring drivers:

1️⃣ Payment History (35%)

On-time payments are the strongest signal in credit scoring models.

2️⃣ Credit Utilization (30%)

Keeping balances below 30% of your limit—ideally below 20%—signals responsible use.

3️⃣ Credit Mix

Adding a revolving account improves profile diversity, especially if you currently have only installment loans.

According to the Consumer Financial Protection Bureau (CFPB), payment consistency and utilization control are the two most influential credit factors.

How Utilization Impacts Your Credit Score

How Long Should You Keep a Rebuilding Card?

One common mistake is upgrading too fast.

Even if your score improves within 6 months, keeping a no-annual-fee card open:

- Strengthens account age

- Improves utilization ratios

- Adds stability to your credit profile

As long as the card has no annual fee, keeping it open long-term is usually beneficial.

According to Experian’s public credit education resources, account longevity contributes positively to overall scoring models.

How to Get Started (Step-by-Step)

Step 1: Check Your Credit Reports

Request your free reports from all three credit bureaus.

Look for errors or outdated negative items.

Step 2: Choose One Card

Applying for multiple cards at once can hurt your score.

Pick the option that best matches your current credit situation.

Step 3: Use Less Than 30% of the Limit

Low balances help your score grow faster.

Even small monthly charges can make a difference.

Step 4: Pay On Time, Every Time

Payment history is the most important credit factor.

Set up automatic payments if possible.

A 6-Month Credit Rebuilding Plan

If you’re serious about rebuilding, follow structure.

Months 1–2: Stabilize

Use the card for one small recurring expense. Keep utilization low.

Months 3–4: Monitor Progress

Check your credit reports at AnnualCreditReport.com to confirm reporting accuracy.

Months 5–6: Evaluate Growth

If your score improves, you may qualify for higher-limit or lower-interest options.

Consistency—not speed—creates measurable improvement.

When a No-Annual-Fee Card May Not Be Enough

In some cases, no-annual-fee cards may still have:

- Low starting limits

- Higher APRs

- Limited upgrade potential

If your goal is aggressive rebuilding, pairing one no-fee card with a secured structure (used responsibly) can diversify your profile.

For example, combining a no-annual-fee unsecured card with a small secured deposit card can strengthen utilization ratios.

That approach works best when applications are spaced responsibly.

Common Mistakes to Avoid

Carrying a Balance Unnecessarily

Interest adds up quickly and doesn’t help your score.

Paying in full is always the safest approach.

Closing Old Accounts Too Soon

Account age matters.

Keep accounts open as long as they have no annual fee.

Falling for “Fast Fix” Promises

Legitimate credit rebuilding takes time.

Cards that report responsibly do more than any shortcut service.

Signs Your Credit Is Actually Improving

Sometimes people rebuild credit but don’t track progress correctly.

Positive signs include:

- Credit utilization below 20%

- No new negative marks

- Increased credit limit offers

- Pre-approval invitations from mainstream issuers

Credit rebuilding is gradual.

But measurable signals appear sooner than many expect.

Choosing the right no-annual-fee credit cards for bad credit is more about long-term stability than short-term approval.

Frequently Asked Questions

How fast can my credit score improve?

Many people see improvement within 3–6 months.

Consistency matters more than speed.

Do secured cards really help credit?

Yes.

They report the same way as unsecured cards when used properly.

Should I avoid rewards cards while rebuilding?

Not necessarily.

Just make sure rewards don’t encourage overspending.

Benefits of Using These Cards

Final Thoughts

No-annual-fee credit cards for bad credit offer one of the safest entry points for rebuilding in 2026.

Rebuilding your credit isn’t about perfection—it’s about progress.

The right no-annual-fee credit card can help you regain financial confidence without adding extra costs.

Stay informed, stay consistent, and make choices that support long-term stability.

Your credit story can always move in a better direction.